It is Possible to do More with Less and Create Greater Value

Have you heard this before?

“As much as I’d like to add another person to your team, we just don’t have the money in the budget. See if you can spread the work across the existing team.”

It’s the constantly-present do more with less mantra. An industry-agnostic challenge that virtually every employee receives at some point in their careers. And as priorities shift, and workloads grow, managers request more from their teams.

But if everything is a priority, which often seems true, then how can employees expect to do their jobs well? Walk through any office and you’ll hear the hectic movements of fingers just trying to get something completed. They check off a box and then it’s onto the next task. It’s no wonder that an important meeting, a report, (a shoe) is likely to drop.

At the heart of every person is a desire to do well. No one wants to be the weakest link on their team. No one wants to perform poorly. But when workloads become unbalanced, it’s not just morale that sinks. The rush to meet deadlines inevitably causes more errors. With a heavy workload and a sprint to every imaginary finish line, leaders need to pause and ask:

CAN YOUR ORGANIZATION TRUST THE INTEGRITY OF THE DATA, OR THE REPORTS, OR THE ANALYSIS YOU’RE GENERATING?

LOSING THE TABOO WITH TECHNOLOGY…

When was the last time you used a physical map to get to a new destination? It’s been a while, right?

Or, the last time you physically dialed someone’s number (by memory!) instead of looking for their name on your cell phone?

The fact of the matter is that we are not only relying on technology more and more, but we are also getting more comfortable using it. There’s a reason we panic when our phone is missing; true, we no longer know those numbers by heart but even truer, our phones literally hold our life’s information!

Think about your own personal use with technology and how it enables you to do things better. AI assistants set timers to ensure meals aren’t overcooked, apps like Waze help us avoid traffic and get to our desired destinations faster, and wrist watches monitor our heart rates to ensure our overall health is on track.

BUT NOT IN THE WORKPLACE

While we are comfortable using technology for personal reasons, when it comes to using it in the workplace, it seems that organizations tend to find every excuse not to invest in it.

Why are some companies so hesitant to invest in technology that would make their employees lives easier? Cost, resources, not enough time?

Think of it this way: if leadership is telling employees to “do more with less,” putting a strong internal system in place is the only way to support and enable those employees to do their jobs.

Can spreadsheets help an employee crunch numbers? Yes. Is it a manual process? Absolutely. Manual processes will continue to put stress on employees and increase the potential for error. Trying to “do more with less” while still using manual processes is the modern-day equivalent of Sisyphus pushing his boulder up the hill; it’s increasingly difficult and every time employees think they get ahead, something will cause the boulder to roll back down.

WHY THE RIGHT SYSTEMS CAN HELP ORGANIZATIONS THRIVE

Strong financial systems can increase productivity, organize business models, and make data useful and readily accessible. Here are three ways the right system can help:

- Create a single source of truth. If companies are not adding to their workforce, they must review proposed processes and workflows to help employees get the information they need. Most companies separate (and silo) finance and accounting departments and therefore store data in multiple locations; as a result, the “do more with less mantra” becomes impossible. By creating a single source of truth, you can empower employees to get the data they need to provide insights and be strategic in their decision-making.

- Understand what companies need to do to grow. Where does your organization want to be in five years? What controls do we need to put in place to make us more successful? Those questions can feel overwhelming to answer. A strong internal system can create a financial baseline that can visualize and “dig into” the data. By doing so, you can see where to adjust and what to focus on for success.

- Generate more time. The whole “do more with less” comes down to time. It bears repeating: At the heart of every person is a desire to do well. Learning a new technology isn’t easy. There’s usually a steep ramp-up to figure out the ins and outs of the system on top of doing your job. Employees feel the pressure and the spotlight on them. Make sure your organization creates a plan to help ease employees’ anxieties and remind them that this new technology will save them time in the long run.

Don’t wait until next year. Organizations are only hurting themselves by waiting to invest in technology. Show your employees that you’re behind them – and the future of the company – by enabling them to do their jobs well. Do more with less may be a mantra for companies, but to their employees, at some point, less will become zero.

Once you have debugged your resource issue, its time to unleash your value creation opportunities.

Dynamic Planning: Unleashing Finance Value Creation

4 IMPORTANT TOPICS TO CONSIDER

Let’s dive deeper into the intent of plan-centered (noun) versus planning-centered (verb).

Budget-centered (noun) organizations respond to changes (e.g. outlook, re-forecast, update) with an updated budget. While important, it’s not nearly as effective as establishing the discipline of planning (verb). If finance organizations become astute at planning, and slowly de-prioritize the ‘completed, term paper’ nature of the budget, they will drive significantly greater Finance Value Creation than those that don’t.

Once finance organizations build planning into their monthly calendar and treat it like an on-going core competency, employees and the organization will need to adopt different thinking. Employees will need to:

- Develop a model-centric mentality

- Understand drivers

- Focus on materiality

- Prioritize Finance Value Creation

LET’S EXPLORE THESE CONCEPTS FURTHER.

1. DEVELOP A MODEL-CENTRIC MENTALITY

Organizations are teams, and high-performing teams efficiently use their time through a good process and constant communication. Having beenpart of an organization where teams wait for the hand-off, I’ve seen the ripple effect. If someone misses a hand-off, a report becomes delayed, the workflow then becomes delayed, and the team misses the deadline.

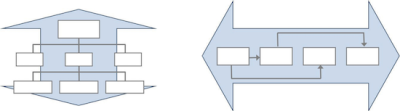

Rather than think of work as a hand-off, we need to start thinking of business as a set of interconnected models that fly in close formation. We know businesses have an overabundance of data, analytics, and data science which are essential to performance and yet, each model is truly independent of the others.

Businesses can categorize each model as a set of inputs, outputs, and business rules.

INPUTS

By and large the inputs are business assumptions that quantitatively articulate the internal and external factors of the business such as:

- number of customers,

- average selling price,

- headcount,

- square footage,

- and many others.

The more effective we are at identifying drivers that ‘live’ higher up in the value chain, the more likely we are to predict financial outputs like revenue, expense, and profit with any degree of accuracy and consistency.

OUTPUTS

The outputs are less defined by the nature of the business, market or economic conditions, but conform to establish GAAP and other modern business standards. Roughly put, this is our common understanding of the P&L and BalanceSheet.

BUSINESS RULES

The business rules in between inputs and outputs can be quite simple or quite complex. For instance, models that calculate less linear functions such as market demand or economic growth attempt to cleanly quantify factors that are not always one hundred percent ‘knowable.’ In these cases, the model reflects a consensus on the best thinking and not a simple answer.

Overtime, data-forward organizations observe and tweak these models while leveraging history and the global marketplace as additional inputs that help fine tune the business rule.

In doing so, S&OP re-imagines the financial view into an integrated horizontal view of the organization that mirrors how raw materials become goods and how the organization then distributes them to the customer. The incredible competitive pressure on organizations in this arena has dramatically streamlined the flow of information both from an actual and forecast perspective.

The shift de-couples the financial view from the traditional management reporting structure and accelerates communication and action to align with the flow of goods. Today’s discussions of driver-based rolling forecasts and integrated business planning seek to leverage this paradigm beyond the tradition flow of manufactured goods and into other industries in efforts to align teams around common KPI’s (key performance indicators) instead of a traditional command-and-control leadership model that is too slow for much of today’s business.

2. FOCUS ON MATERIALITY

Materiality is a major sticking point in organizations where finance doesn’t trust their business counterparts’ aptitude or honesty in the planning process. Companies typically structure expense planning as a zero-based, bottoms-up exercise that requires budget owners to develop and justify spend by line item. Function leaders navigatethrough a cycle of mistrust by goal-seeking and the invention of needs in preparation for a negotiation with corporate finance.

It often fails to accomplish three critically important goals of a healthy planning process.

- ALIGN CONTROL WITH AUTHORITY. One-sided budget conversations fuel a sense of distrust and dilute ownership. It’s truly a win-lose, or more likely lose-lose proposition. When leadership trusts a budget manager to make good decisions on resource allocation, they create a true win-win opportunity.

- DEFINE EXPECTATIONS BY LEVERAGING HISTORY AND ACCEPTED RATIOS. The greatest indicator of future performance is historic performance. Historic driver and financial data and the trends within should always be the starting point of a planning conversation. A follow-on study of the fundamental business changes and their financial impact becomes the storyline for budget approval.

EMPOWER THOSE OF THE FRONTLINES WITH THE CREATIVE PROCESS OF DOING AS MUCH AS POSSIBLE WITH AS LITTLE AS POSSIBLE. Those in the weeds daily know your data best. Allow them to analyze the data and translate what they see to leadership. By allowing them to visualize trends, you are empowering them to feel that they are making an impact at the organization. All employees want recognition for good work and this gives them a chance to advance initiatives and spark ideas.

Finance doesn’t hire smart, degreed people to simply consolidate spreadsheets, tick and tie results, and update PowerPoint presentations. And yet, sadly, too often that is exactly what consumes most of their time.

The data is clear. Finance organizations that invest more on finance-focused technology have a smaller, more highly paid team and excel on finance value creation metrics. The more time finance spends on addressing the CFO’s core concerns, instead of preparing data and reports, the stronger the team—and the insights—will be. Here’s a summary of core CFO concerns:

- Survive disruption

- Raise prices

- Drive a culture of data (that’s us!)

- Execute crisply

- Increase margins

- Invest for growth

Much of the Enterprise Performance Management (finance-focused technology) market exists as a unification of acquired software platforms that sit on different technology and rarely address all the needs a finance organization. Sadly, the largest players are not necessarily investing in this type of innovation; instead, they seem to mainly focus on moving customers to the cloud as quickly as possible.

There are some emerging vendors, however, who are now re-building this suite of solutions (e.g. Financial Close, Consolidation, Account reconciliation, Disclosure and reporting, Budgeting, Forecasting, Analytics, etc.) on a unified database with a fully integrated suite of applications. As your organizations spends money on EPM going forward, ensure your investments are going toward product innovation and not just cloud migration.

Already a Member? Login HERE.

Identify your path to CFO success by taking our CFO Readiness Assessmentᵀᴹ.

Become a Member today and get 30% off on-demand courses and tools!

For the most up to date and relevant accounting, finance, treasury and leadership headlines all in one place subscribe to The Balanced Digest.

Follow us on Linkedin!